The transition for an investor from the accumulation and growth phase of their career, to the distribution phase of retirement, is associated with multiple changes. The goal for the investor changes from contributing to savings and exposure of assets to capital markets at an appropriate level of risk in order to accumulate assets for retirement, to targeting specific cash flows that will be generated from a number of possible sources, which together will provide a safe and secure income stream through retirement.

During the retirement phase, the investor has access to financial products like fixed income and variable annuities that can be used for generating retirement income. The investor must also make tax-sensitive decisions like the timing and order of withdrawal across tax-type accounts and the accounts to use for the purchase of the annuities.

The composition of the portfolio between investment products and annuities, the level and timing of annuity purchases, and ordering of withdrawals across all income sources taken together constitute a retirement income strategy.

How does an investor know which income strategy is the most appropriate? A basis of comparison is needed to clearly judge the effectiveness and weakness of multiple retirement income strategies. Income Discovery proposes a new risk-reward analysis framework that complements traditional volatility-return based risk-reward frameworks used for the accumulation and growth phase of an investor. The metrics that make the framework are described below:

Reward #1 – Retirement Income

Similar to the reward of expected return for an investor interested in growing the portfolio, the reward for a retiree is the level of inflation-adjusted retirement income. If a particular strategy can generate higher retirement income with similar risk, it is deemed a better strategy.

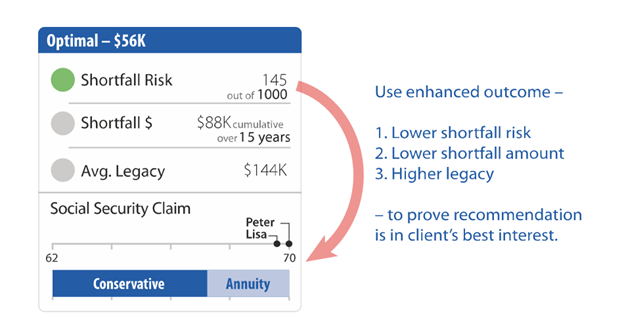

Risk #1 – Number of Shortfall Retirees (Shortfall Risk)

The first risk for the retiree is that the assets may not last for the planned horizon. A situational analysis of one thousand hypothetical retirees that have the same asset base and follow the same strategy as the investor, but get exposed to different sequences of inflation and asset returns, is first conducted by the application. Out of those one thousand retirees, the number who experienced a shortfall over the plan term are identified and communicated to the client as a measure of risk.

Risk #2 – Cumulative Shortfall for Unfortunate Retiree

Knowing how many investors out of one thousand fell short of having enough assets to carry them through retirement, viewed alone, doesn’t complete the risk picture, and may, in fact, give a false sense of comfort to the client. We need to ask the additional question – “What was the magnitude of shortfall for these individuals.” Here’s why: certain strategies, such as the use of a portfolio with higher return and corresponding higher volatility, may increase the number of retirees with full income but in doing so such a strategy could also raise the magnitude of shortfall in catastrophic market conditions.

The magnitude of shortfall is observed by calculating the cumulative shortfall for each hypothetical retiree who ran out of retirement funds during retirement. “Shortfall” refers to the percentage gap from the desired income in each year. For each hypothetical retiree, the shortfall is accumulated over all the years. Out of the one thousand hypothetical retirees, the retiree whose cumulative shortfall over the planning horizon is ranked 20th from the top is termed the Unfortunate Retiree.

For that Unfortunate Retiree, the cumulative shortfall is also captured in dollars—and that becomes the second risk metric of the framework. For additional clarity, the number of years the shortfall is experienced by the Unfortunate Retiree is also communicated.

Reward #2 – Average Legacy

After having satisfied the primary goal of generating the retirement income within acceptable risk, the secondary goal for the retiree is leaving a legacy. The median value of the 1000 portfolios at the end of the planning horizon captures the secondary goal, and becomes the second reward metric of Average Legacy in the proposed analysis framework. It is measured in purchasing power of today's dollars.

Resources:

An earlier version of this framework was also published in the Journal of Financial Planning (link).

Also read how behavioral finance research led us to come up with the above form of metric presentation at Presenting Plan Performance as Story, Not as Statistics.

0 Comments